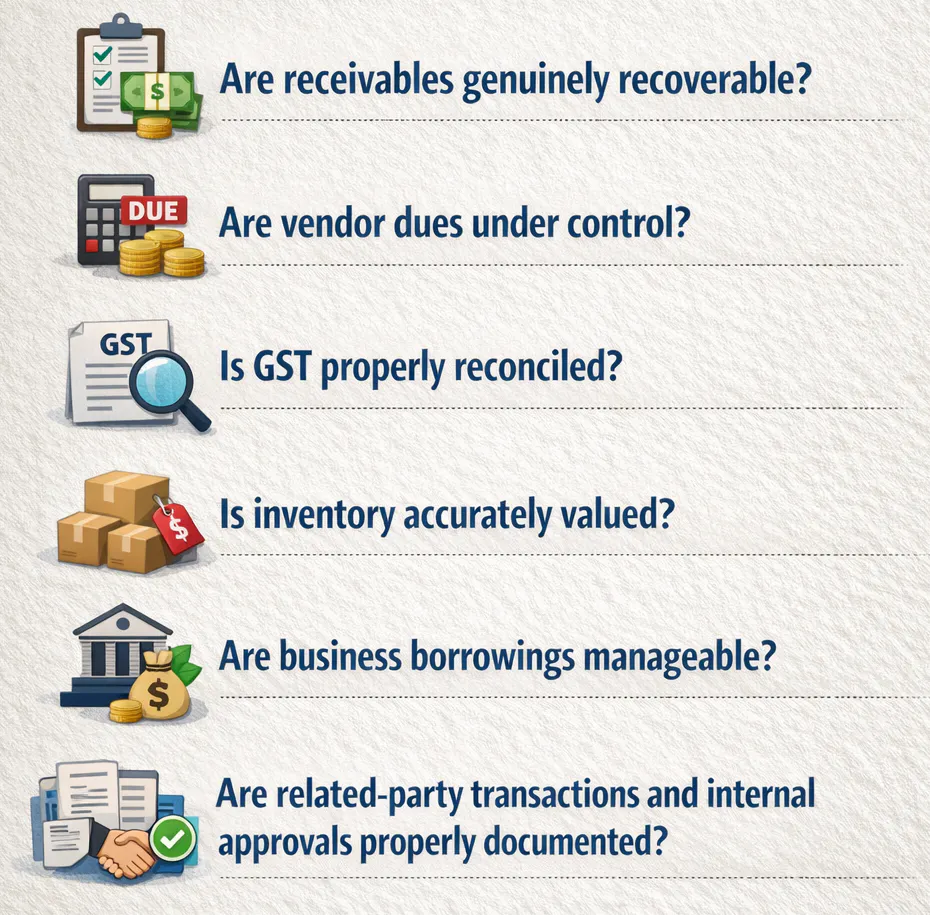

What MSMEs Should Review Before 31st March

Financial Leadership and Governance

As the financial year draws to a close, many MSME founders become intensely focused on sales, collections, vendor payments, tax filings, and year-end closures. While these are all important, 31st March should not be viewed merely as an accounting deadline. It is, more importantly, a leadership milestone.

For any founder, year-end is the right time to step back and ask a few hard but necessary questions.

These questions go beyond accounting. They go to the heart of financial discipline, MSME governance, and business sustainability.

Cash Flow Review (MSME Liquidity & Working Capital Management)

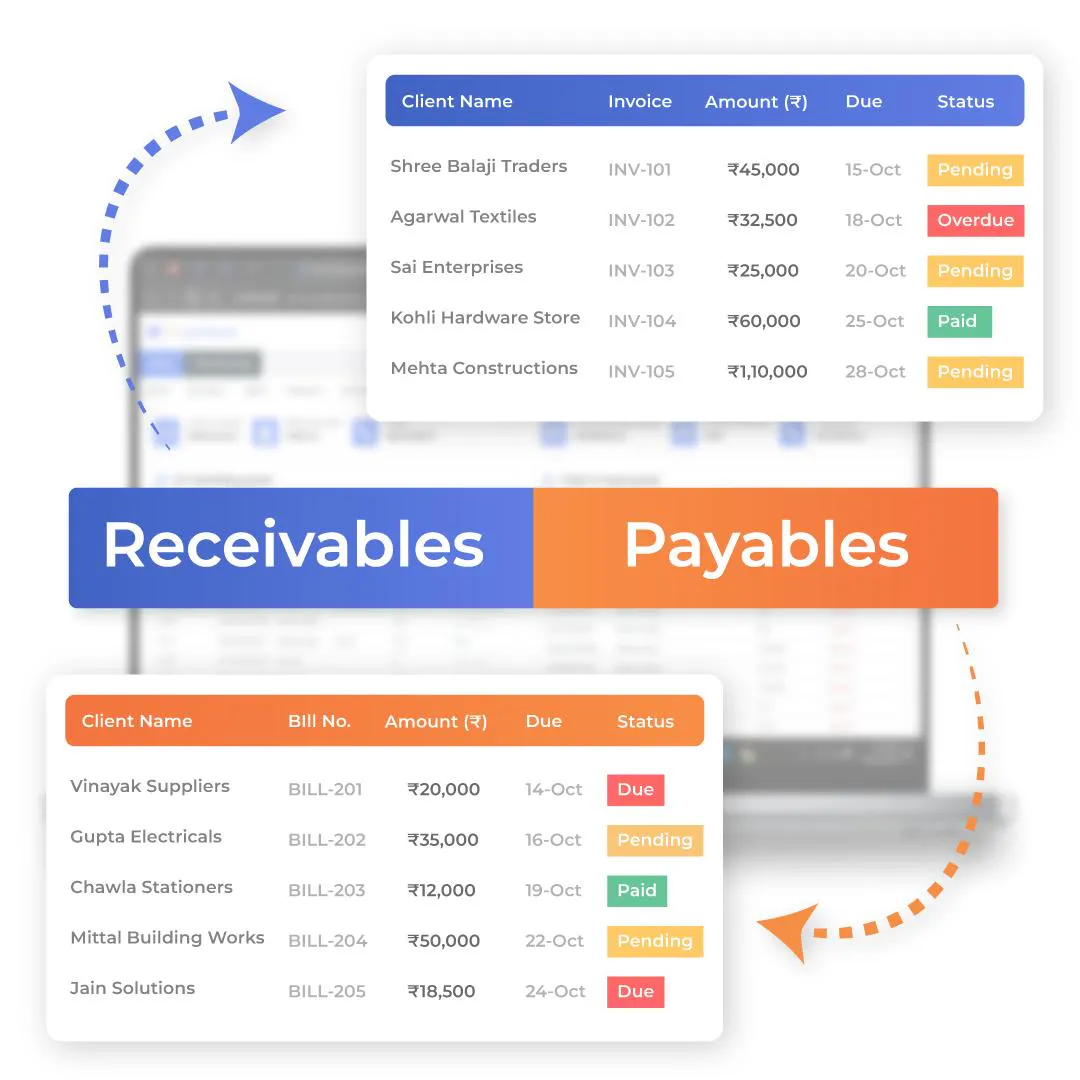

The first review area should be cash flow. Many MSMEs report profits in the books but struggle with liquidity in practice. Profit does not always translate into cash. Therefore, founders must review debtor ageing, blocked funds in inventory, and overdue payables. A realistic look at collections often reveals the true health of the business. If receivables are old, disputed, or unlikely to be realised soon, that must be acknowledged honestly before stepping into the next financial year.

Vendor Payments & MSME Compliance (MSME Act, Creditor Management)

The second area is vendor payments, especially dues payable to micro and small enterprises. This is a significant year-end review point. Businesses should identify which vendors fall under the MSME category and separately monitor outstanding balances due to them. Delayed payments can create both legal and tax implications. Yet many businesses still maintain a single undifferentiated creditor list. That approach is no longer sufficient. A well-governed MSME should know exactly which dues are sensitive, which are ageing, and which require immediate action before year-end.

GST Reconciliation (GST Filing, Input Tax Credit, Compliance)

GST is the third area that deserves close attention. Too often, founders leave GST clean-up to consultants at a later stage, only to discover mismatches when annual reconciliations begin. Before 31st March, turnover as per books should be compared with GSTR-1 and GSTR-3B. Input tax credit mismatches, missing supplier filings, incorrect treatment of credit notes or reverse charge transactions, and ineligible credits should all be reviewed. GST issues are not merely compliance matters; they affect working capital, margin visibility, and credibility.

Inventory Management (Stock Valuation & Verification)

The fourth review area is inventory. In many MSMEs, inventory is one of the most misunderstood figures in the financial statements. Stock may be slow-moving, obsolete, damaged, or commercially irrelevant, yet still carried at values that make the business appear stronger than it is. A good year-end review should classify stock into moving, slow-moving, non-moving, and obsolete categories. Physical verification and reconciliation with records are equally important. Founders must ensure that the stock reflected in the books is both real and saleable.

Debt & Borrowings (Business Loans, EMI Planning, Financial Risk)

Debt and borrowing should be the fifth area of review. Many businesses continue repayment schedules without truly evaluating whether the debt structure remains sustainable. At year-end, management should review outstanding principal, EMI commitments, penal interest, securities offered, and personal guarantees. If debt servicing depends on delaying vendor payments, stretching receivables, or regular promoter support, this indicates more than financial pressure. It points to a structural governance concern that deserves immediate attention.

Legal & Documentation Review (Contracts, Agreements, Risk Management)

Seventh, legal and commercial documentation should be examined. Many businesses continue operating on informal understandings without updated agreements, work orders, acknowledgements, or renewal records. Founders should use the year-end period to identify missing contracts, unresolved disputes, unsigned arrangements, and pending notices. Several future problems arise not because the business lacked activity, but because it lacked documentation.

Year-End Governance Review (Business Strategy & Financial Planning)

Finally, every MSME should hold a simple but structured year-end governance review. This need not be highly formal, but it should cover the essentials: receivables, payables, MSME dues, GST status, inventory, debt, related-party items, pending notices, and major decisions required before entering the next financial year. A brief internal note or meeting summary can itself become evidence of sound management discipline.

Conclusion (MSME Financial Strategy & Leadership)

To conclude, 31st March should not be treated only as a closing date. It should be treated as a control date. The best MSMEs are not those that merely close the year quickly, but those that enter the next year with clarity, discipline, and accountability. Financial leadership is not only about growth. It is also about control, foresight, and well-timed decisions.

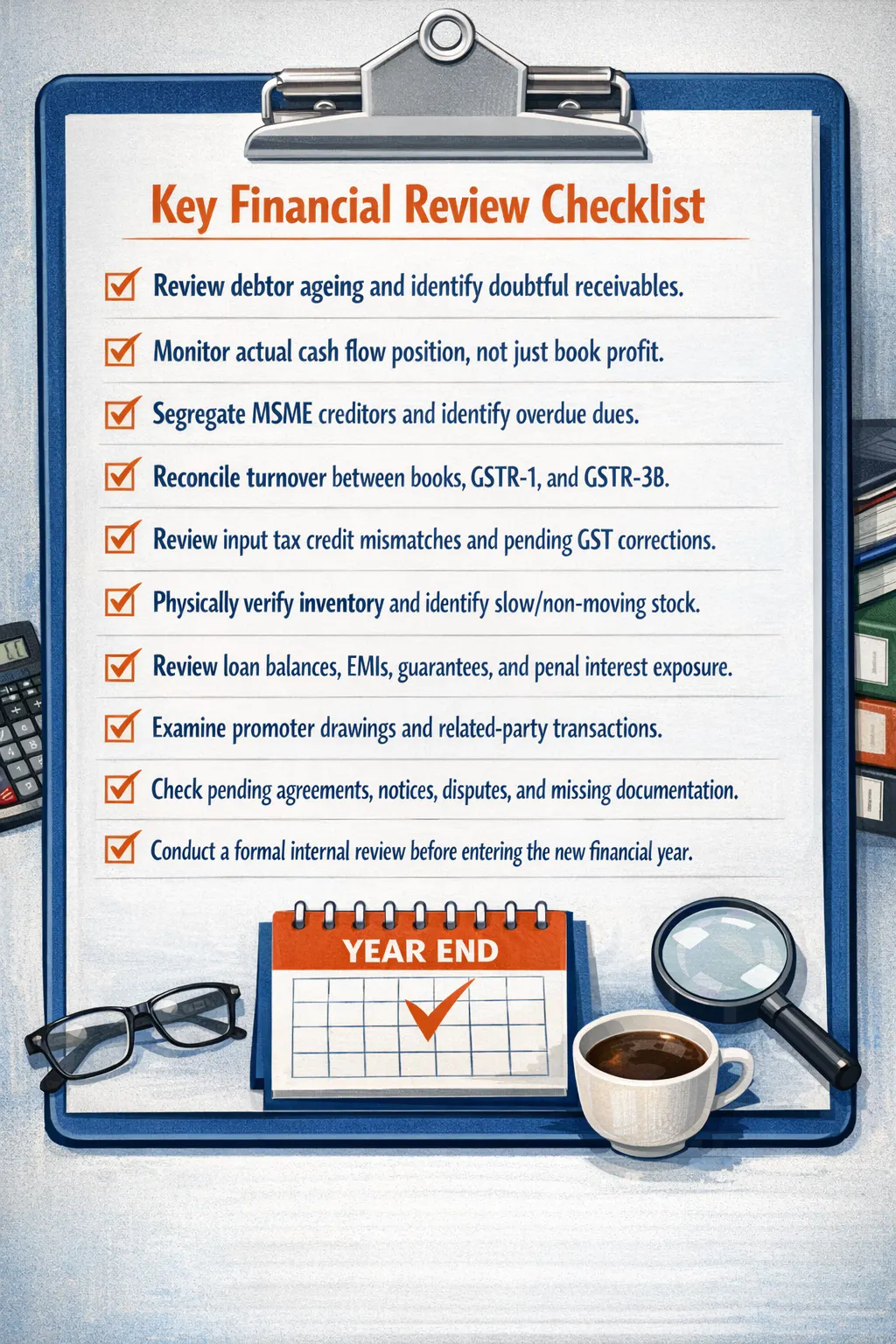

10-Point Year-End Founder Checklist (MSME Compliance Checklist)

About the Author

Vijay Ponneri is a finance and compliance specialist serving NGOs, churches, and mission-driven organizations. With 20+ years of expertise across audit, taxation, FCRA, and legal frameworks, he equips leaders with governance clarity, ethical processes, and value-based financial stewardship.